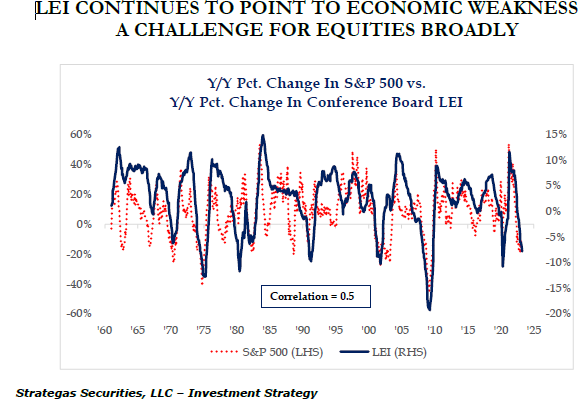

- The Conference Board Index of Leading Economic Indicators (LEI) fell in March for the twelfth monthly decline, now down 7.8% year over year. This is a magnitude never seen outside of recessions.

- As a recession gauge, continuing unemployment claims are a somewhat better indicator than the headline initial jobless claims. As of the week of April 10th, continuing claims were up 22.1% from the year earlier. Any rise in continuing claims greater than 10% on a year-over-year basis has never occurred outside of a recession.

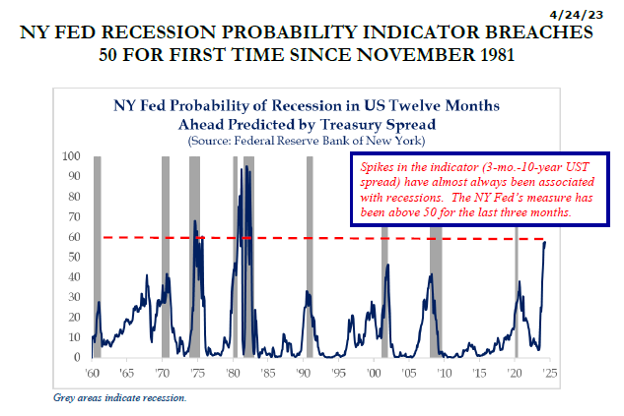

- We have discussed inverted yield curves and their predictive power in past blogs. The New York Federal Reserve uses a ‘recession probability indicator’ which is their proxy for an inverted yield curve. It is defined as the three-month Treasury bill yield minus the 10-year Treasury note yield. As you can see in the chart below, spikes in this indicator have been associated with recessions.

- There has never been an inverted yield curve setting that did not also foreshadow a recession in corporate profits.

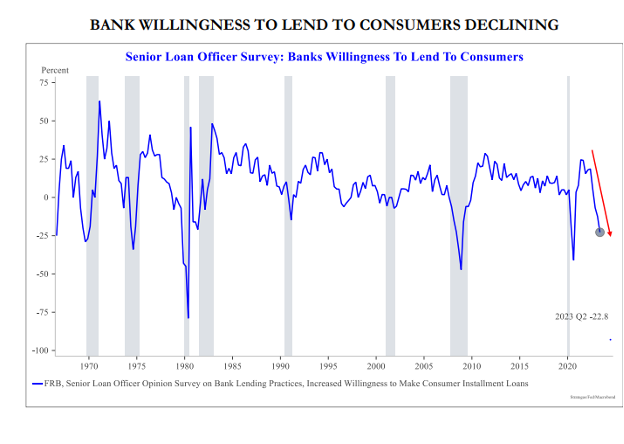

- The Fed’s most recent Senior Loan Officer’s Survey (SLOS) showed a further tightening of already recessionary lending standards in this quarter. Changing lending standards are a good predictor of future bank lending and corporate revenues. So, one would expect both to decline significantly by year-end.

“Policymakers often talk about default on the U.S. debt during debt ceiling debates, but the threat of an actual default of the U.S. debt is an extremely low probability. We (believe) this is a political argument designed to pressure the other side into moving forward on the debt ceiling and/or their preferred attached policies. In reality the U.S. government has more than enough cash flow to pay interest even if the ‘default date’ is reached.

Should Congress fail to raise the debt ceiling, the government would have enough money for Social Security, Medicare, Defense, and interest. Other government spending would come to a halt, which is akin to a government shutdown.

In this current cycle, the prioritization of government spending would be short lived, as the Treasury expects new tax revenue on June 15th and new extraordinary item cash on June 30th, which can cover through the end of July. As such, we see little chance of default even if Congress does not act.

The debate right now is “how” to raise the debt ceiling, not “whether” and that is an important distinction. In our view, the most likely outcome would be a cap on discretionary spending, rescinding of unspent COVID funding, and energy permitting reform…(it) is not a straight line. Policymakers may fail before they succeed.”

The material included herein is not to be reproduced or distributed to others without the Firm’s express written consent. This material is being provided for informational purposes, and is not intended to be a formal research report, a general guide to investing, or as a source of any specific investment recommendations and makes no implied or express recommendations concerning the manner in which any accounts should be handled. Any opinions expressed in this material are only current opinions and while the information contained is believed to be reliable there is no representation that it is accurate or complete and it should not be relied upon as such. Investing involves risk, including loss of principal, and no assurance can be given that a specific investment objective will be achieved.

The Firm accepts no liability for loss arising from the use of this material. However, Federal and state securities laws impose liabilities under certain circumstances on persons who act in good faith and nothing herein shall constitute a waiver or other limitation of any rights that an investor may have under Federal or state securities laws.

2x Wealth Group is a team at Ingalls & Snyder, LLC.,1325 Avenue of the Americas, New York, NY 10019-6066 | (212) 269-7757