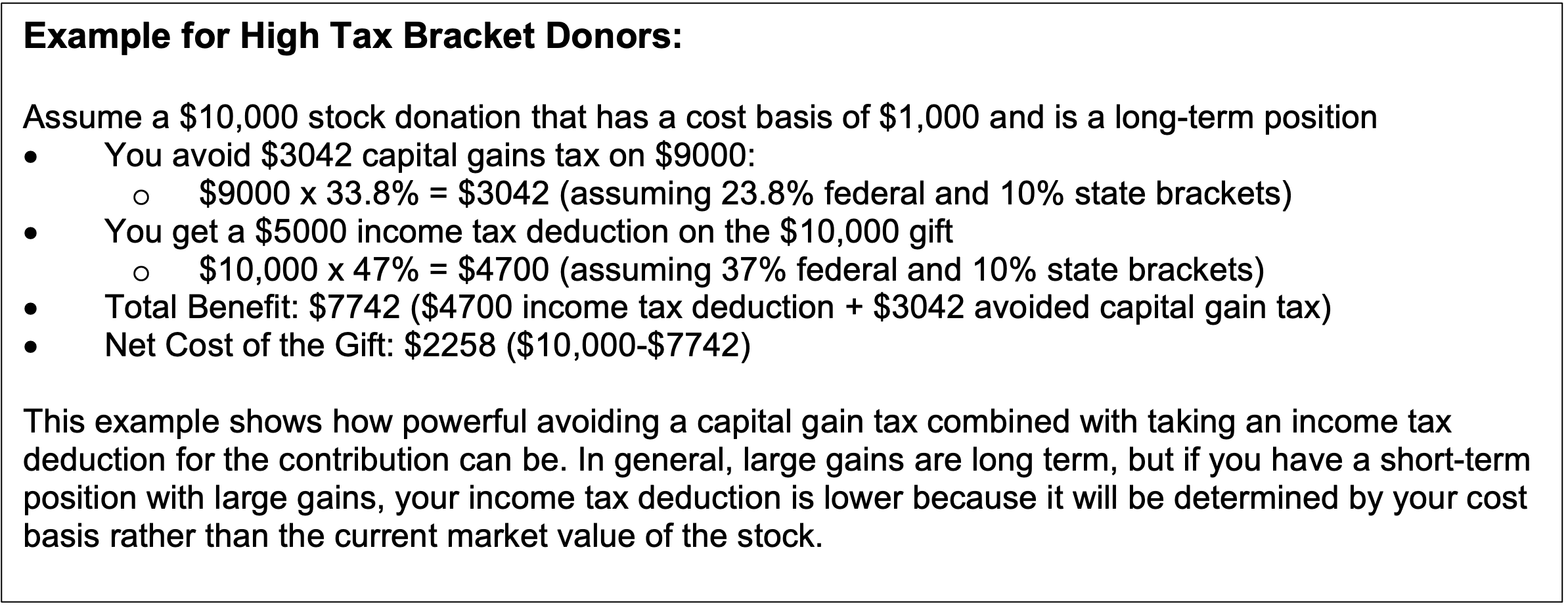

Charitable giving with appreciated stock can be one of the best ways to support causes you care about. Donating highly appreciated stock combines philanthropy, tax efficiency, and tactical portfolio management in a single move. You can take a charitable deduction based on the current market value (subject to IRS rules) of your stock, typically avoid capital gains tax, and simultaneously trim concentrated or overweight positions in your portfolio.

- When selling appreciated stock, you recognize capital gains on the difference between the amount you paid and the amount you sell it for.

- Alternatively, when donating appreciated stock, you can generally deduct the current market value of the shares from your income, subject to adjusted gross income (AGI) limits. Income limits are often 30% of AGI for gifts to public charities.

- With this strategy, you sidestep the capital gains tax you would have owed if you sold first and gave cash from the sale instead.

- Since charitable organizations do not pay capital gains tax, the full market value of your donation can be used.

Why Earlier in the Year Giving Can Make Sense

Many people bunch charitable planning into year end, but if you are specifically worried about a certain stock or ETF underperforming, there is a strong case for making your contribution earlier. By reducing concentration sooner, you can redeploy equity risk into assets you like better, rather than carrying an overweight position when you expect relative underperformance.

- Confirm whether you are donating short or long-term (held > one year) appreciated stock. The tax consequences are different. When donating long term positions you can deduct the full market value. For short-term holdings, you can only deduct the cost basis. In both cases, no capital gains tax is paid, but if you donate short term holdings, you waste the value of the appreciation from a tax standpoint.

For example: If you bought a stock for $10,000 which is now worth $100,000 eight months later, your deduction would be $10,000. If you waited and sold it when held for a year, your deduction would be $100,000. However, it might still make sense if you really wanted to reduce your position now because of market risk. - Check AGI limits and potential carryforwards with your tax advisor; large gifts can create multi-year deduction carryovers.

- A donor-advised fund can be an efficient hub for giving: you transfer appreciated stock once, take the deduction now, and then make grants to charities over time. AGI limits apply for how much you can deduct in a single year.

Donating directly from your IRA can be especially useful if you don’t need the money to live on. If you make a Qualified Charitable Distribution (QCD), you can transfer money straight from your IRA to a qualified charity. The amount of the gift counts toward your RMD but is not included in your taxable income. In effect, you satisfy the requirement to withdraw funds without increasing your tax bill.

Important Considerations

- In 2026, the QCD limit is $111,000 per person. Married couples, each with their own IRA, can contribute $111,000 each.

- You can make a QCD starting at age 70 ½ even though you are not yet required to take an RMD.

- QCDs are not counted toward the ‘maximum amounts deductible’ for those who itemize charitable giving on their tax returns. This feature means a QCD can potentially allow for a larger charitable gift than otherwise possible if you simply donate cash or other assets.

The material included herein is not to be reproduced or distributed to others without the Firm’s express written consent. This material is being provided for informational purposes, and is not intended to be a formal research report, a general guide to investing, or as a source of any specific investment recommendations and makes no implied or express recommendations concerning the manner in which any accounts should be handled. Any opinions expressed in this material are only current opinions and while the information contained is believed to be reliable there is no representation that it is accurate or complete and it should not be relied upon as such. Investing involves risk, including loss of principal, and no assurance can be given that a specific investment objective will be achieved.

The Firm accepts no liability for loss arising from the use of this material. However, Federal and state securities laws impose liabilities under certain circumstances on persons who act in good faith and nothing herein shall constitute a waiver or other limitation of any rights that an investor may have under Federal or state securities laws.

2X Wealth Group is a team at Ingalls & Snyder, LLC., 1325 Avenue of the Americas, New York, NY 10019-6066. If you would like to unsubscribe, please click here.