What Causes Banks to Fail

How the Government is Responding

How Bank and Brokerage Accounts May Be Protected

Dilemma for the Federal Reserve

In light of the sudden failure of Silicon Valley Bank, followed by the failure of Signature Bank of New York, and the teetering condition of a few other regional banks, we wanted to show how banks work, why they fail and how the government is responding. We explain in detail how bank and brokerage accounts may be protected by insurance. Finally, we discuss how the recent bank events cause a dilemma for the Federal Reserve regarding its goal to slow inflation.

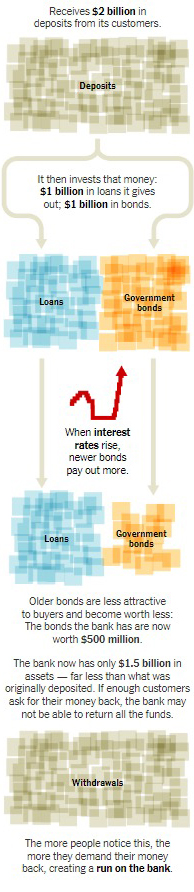

To understand how a bank works, this picture from the New York Times, on March 18, 2023, is worth a thousand words.

All was good as long as SVB only had to pay their customers very low rates for deposits. The whole situation started to unravel when the Federal Reserve started raising interest rates in March 2022 leading to the following chain of events:

- Technology stocks fell in value and companies no longer issued stock to raise cash. So, instead of growing, SVB deposits shrank as companies used their available deposits to run their operations.

- Short term interest rates rose substantially thanks to the Fed, forcing SVB to pay their customers higher interest rates in order to keep their deposits.

- The value of SVB’s long-term bond portfolio fell substantially as long-term interest rates went up. Bond prices go down as interest rates rise.

- SVB was forced to sell bonds (at a loss) to raise money that depositors requested. Once venture capital firms became aware of the losses, they told their startup companies who banked at SVB to take money out immediately.

- There was a run on the bank as too many customers withdrew their money at once ($42 billion on Thursday, March 9, 2023!) before SVB could address the problem by raising more capital.

Certain amounts of your bank deposits are covered by the Federal Deposit Insurance Corporation (FDIC). The FDIC was created by Congress in 1933 during the Great Depression to maintain stability and public confidence in the U.S. financial system. The amount of FDIC insurance increased from $100,000 to $250,000 per ownership category (e.g., joint tenant, individual or IRA) in 2008 during the Great Recession. A lesser-known feature of FDIC insurance is that a POD (Payable on Death) bank account with beneficiaries can increase FDIC coverage. Since coverage under FDIC is based on individual circumstances, you should consult with each individual financial institution to inquire about coverage amounts based on your specific deposit amounts and account types.1

To maintain high cash deposits, it may be prudent to:

- Spread the wealth among different banks to mitigate the concentration risk at a single bank that may experience distress.

- Have different types of accounts at any bank to ensure that your deposits are fully covered under FDIC rules for coverage (e.g., joint tenant, individual or IRA).

- Inquire with your financial institution/financial advisor to determine whether opening POD (Payable on Death) bank accounts make sense in your individual situation.

- Keep in mind, cash in money market mutual funds currently offers similar liquidity and much higher interest rates than bank deposits.

2X Wealth Group custodies our clients’ accounts at Charles Schwab. For the purposes of this blog, we will use Charles Schwab as an example. Unlike accounts at a bank that are covered under FDIC insurance, securities accounts at broker dealers such as Schwab are covered by the Securities Investor Protection Corporation (SIPC) which provides protection for both securities and cash in client brokerage accounts.

- SIPC protections are activated in the rare event that the broker-dealer fails and client assets are missing due to fraud or other causes. According to SIPC, most broker-dealer failures happen with no securities missing. Since SIPC’s inception over 50 years ago, 99% of eligible investors got their investments back in the failed brokerage firms cases that it has handled.

- SIPC coverage is used to make investors whole if there is a shortage after all customer assets held at the brokerage firm have been recovered. SIPC provides up to $500,000 of protection for brokerage accounts held in each separate capacity (e.g., joint tenant, individual or IRA), with a limit of $250,000 for claims of uninvested cash balances.

- Investments at Schwab are segregated at the broker/dealer which means these assets are separate and not commingled with assets at Schwab Bank.

- These segregated assets are protected against the broker/dealer creditors’ claims.

- For cash held at Schwab Bank, clients have FDIC insurance up to the limit.

- Schwab has a very safe and liquid balance sheet.

- In addition to SIPC, Schwab clients receive an extra level of coverage through "excess SIPC" insurance protection for securities and cash. This helps ensure claims will be covered in the event of a brokerage firm failure and funds covered by SIPC protections are exhausted. The combined total of Schwab’s SIPC coverage and Schwab’s "excess SIPC" coverage means Schwab provides protection up to a combined return of $149.5 million per customer, up to $1.15 million of which may be in cash. The Excess SIPC program has a $600M aggregate (meaning the most the program will pay for the Excess SIPC portion of the losses). Commodity interests and cash in futures accounts are not protected by SIPC.

The material included herein is not to be reproduced or distributed to others without the Firm’s express written consent. This material is being provided for informational purposes, and is not intended to be a formal research report, a general guide to investing, or as a source of any specific investment recommendations and makes no implied or express recommendations concerning the manner in which any accounts should be handled. Any opinions expressed in this material are only current opinions and while the information contained is believed to be reliable there is no representation that it is accurate or complete and it should not be relied upon as such. Investing involves risk, including loss of principal, and no assurance can be given that a specific investment objective will be achieved.

The Firm accepts no liability for loss arising from the use of this material. However, Federal and state securities laws impose liabilities under certain circumstances on persons who act in good faith and nothing herein shall constitute a waiver or other limitation of any rights that an investor may have under Federal or state securities laws.

2x Wealth Group is a team at Ingalls & Snyder, LLC.,1325 Avenue of the Americas, New York, NY 10019-6066 | (212) 269-7757