- Falling stock and bond prices

- Higher mortgage rates

- Decreased home prices and sales

- Falling job openings

- Constant media focus on recession and recession risk

Recessions can also happen in response to significant world events such as:

- Demobilization after WWII - going from a war economy to a peacetime economy

- The OPEC oil embargo in 1973-75 and President Nixon’s wage-price controls

- The COVID pandemic in 2020

- An inverted yield curve. If the 3-month Treasury bill yield rises above the 10-year Treasury note yield for several months, a recession happens most of the time. See our prior blog on the shape of the yield curve.

- The unemployment rate rises half a percent above the year ago level. Any rise of this magnitude or more has been a signal that the economy is either in a recession or on the cusp of one, with no exceptions in post-war history.**

- Falling real income – personal income adjusted for inflation goes down substantially.

- The Federal Reserve has raised interest rates at the fastest pace in the last 35 years.

- In periods where the Fed is hiking and food and energy inflation rose above 5%, the economy has always gone into recession.***

- Every time we have had unemployment below four percent and inflation above four percent, we have had a recession within the next two years****.

- Money supply growth has fallen dramatically, a typical precursor to recessions. Real M2 (a common measure of money supply) is the most negative since the 1973-74 recession and bear market.

- Consumer expectations have declined 10% - history has shown drops of this level lead to recessions.

Inflation. Persistent inflation can affect the severity of a recession if it causes the Fed to be more restrictive for longer.

Housing may suffer less. After the 2008/9 housing crisis, many homebuilders went out of business and underbuilt housing for a decade. “America's fallen 3.8 million homes short of meeting housing needs… and that's both rental housing and ownership” according to the nonprofit group Up for Growth (July 2022). Lack of supply may put a floor under the housing market.

Unlike typical recessions, we think inflation will persist (see our recent inflation blog). There will likely be similarities to the slow growth, persistent inflation of the 1970s and early 1980s, but without the spikes in unemployment which rose as high as 10.8% in 1982.

- Price/earnings multiples come down as interest rates rise, i.e. the amount of money people are willing to pay for a company’s earnings falls. So far this year, multiples have fallen from 22 P/E to 16 P/E, partly due to inflation.

- Value stocks tend to outperform growth stocks. Value stocks typically have current cash flow which is worth more to investors than growth stocks whose cash flows may be far out in the future.

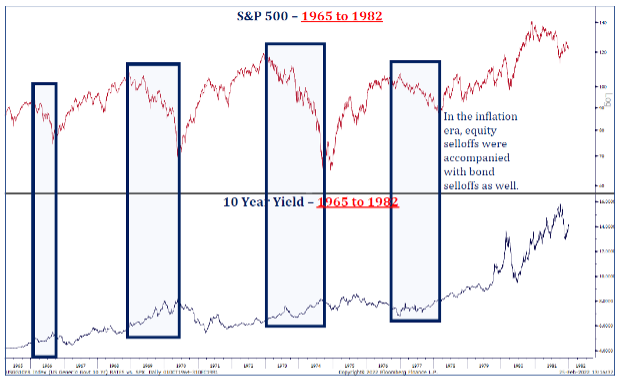

- Stock and bond markets both go down. Bond prices fall as yields increase.

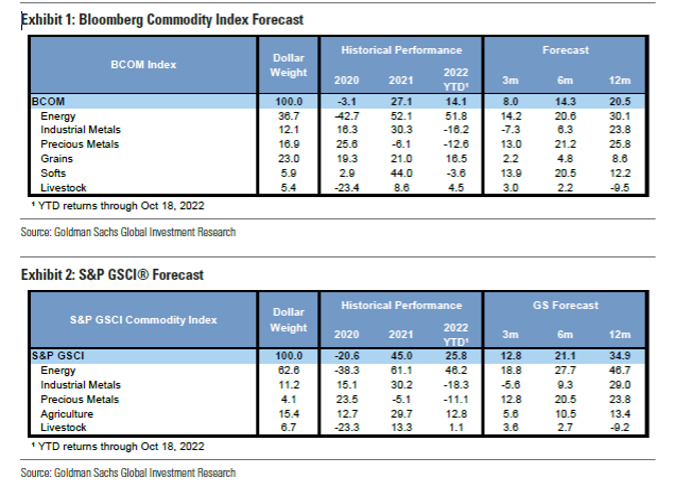

- If inflation is present, commodity stocks tend to outperform, particularly if recessions follow a period of capital underinvestment by commodity companies. The chart below shows how commodities have performed in 2021 and YTD 2022. This year, energy and agriculture commodities went up even when the S&P declined.

- The Fed achieves its policy goals - in this case lowering inflation.

- Something breaks - a large institution or country runs into a financial problem that creates systemic risk for markets and the economy. Think of the housing crisis in 2008/09.

- The stock market abruptly tanks – think end of 2018.

- Value ETFs or mutual funds

- Health Care stocks/ETFs – for defensive positioning as healthcare is always needed

- Dividend growth stocks/ETFs – for high quality companies with cash flow

- Energy stocks/ETFs – for exposure to commodities with scarce supply vs. demand

- We have a high chance of going into a recession.

- Recessions are a sustained slowdown in economic growth characterized by slowing gross domestic product (GDP), falling income and rising unemployment.

- Recessions are most often caused by the Federal Reserve slowing down an overheated economy but can also be caused by significant events like the pandemic.

- If we have a recession, we think unemployment will rise less and housing will hold up better than typical recessions. This recession will likely have similarities to the recessions in the 1970s and early 1980s where inflation persisted.

- Recessions end when economic growth returns, typically when the Federal Reserve lowers interest rates to stimulate growth. Investors try to anticipate renewed growth by buying stocks.

[2] The Strategic Petroleum Reserve, established by Congress in 1973 after the OPEC oil embargo “to reduce the impact of energy supply disruptions.”

[3] The world’s six or seven largest publicly traded and investor-owned oil companies

The material included herein is not to be reproduced or distributed to others without the Firm’s express written consent. This material is being provided for informational purposes, and is not intended to be a formal research report, a general guide to investing, or as a source of any specific investment recommendations and makes no implied or express recommendations concerning the manner in which any accounts should be handled. Any opinions expressed in this material are only current opinions and while the information contained is believed to be reliable there is no representation that it is accurate or complete and it should not be relied upon as such. Investing involves risk, including loss of principal, and no assurance can be given that a specific investment objective will be achieved.

The Firm accepts no liability for loss arising from the use of this material. However, Federal and state securities laws impose liabilities under certain circumstances on persons who act in good faith and nothing herein shall constitute a waiver or other limitation of any rights that an investor may have under Federal or state securities laws.

2x Wealth Group is a team at Ingalls & Snyder, LLC.,1325 Avenue of the Americas, New York, NY 10019-6066 | (212) 269-7757